WinSavvy Editorial Standards

How this article was created

Buying a home is one of the biggest decisions a person will ever make. It is not like buying a phone, booking a trip, or choosing a new pair of shoes. A home loan affects a family’s savings, monthly budget, future plans, and sense of safety. That is why people do not choose a lender only because they saw one ad or found one low rate. They choose the brand they trust most.

Build Your Home Loan Marketing Around Trust Before You Sell Anything

Home loan customers do not wake up one morning and suddenly decide to apply for a loan. Most of them spend weeks or even months thinking, comparing, worrying, asking friends, checking prices, and trying to understand what they can afford.

By the time they contact a lender, they have already formed strong opinions about who feels safe and who feels risky.

That is why trust must come before the sale.

If your marketing only says “low rates,” “quick approval,” or “apply now,” you are entering the customer’s mind too late. You are speaking to them as if they are ready, when in reality, many are still trying to understand the road ahead.

They want answers before offers. They want confidence before forms. They want proof before promises.

A strong home loan marketing strategy starts by becoming useful long before the customer is ready to apply.

Your customer is not just comparing rates, they are comparing risk

When someone looks for a home loan, they are not only asking, “Who has the lowest rate?” They are also asking, “Will this company guide me properly?” “Will they hide charges?” “Will they reject me after wasting my time?” “Will I understand what I am signing?” “Will I regret this later?”

These questions are emotional. They are not always spoken out loud. But they shape every click, call, and decision.

So your marketing must reduce fear. Every page, ad, email, video, and sales message should make the buyer feel more informed and less alone. This is especially important for first-time buyers. They may not know what documents are needed.

They may not understand fixed rates, floating rates, processing fees, prepayment terms, loan tenure, or eligibility rules. If your brand explains these things in simple words, you become more than a lender. You become a guide.

That position is powerful.

Because when the customer finally becomes ready to apply, they are more likely to choose the brand that helped them understand the journey.

Speak to the fear behind the search

A person searching “best home loan near me” may look like a hot lead. But behind that search, there may be fear. They may be worried about rejection. They may be worried that their salary is not enough. They may be unsure whether they should buy now or wait. They may be confused by different lender offers.

Your content should speak to these hidden fears directly.

Instead of only writing a page titled “Best Home Loan Offers,” create content that answers the real worry behind the search. For example, write about how to know if you are ready for a home loan, what banks check before approving a loan, how to avoid choosing the wrong loan tenure, and what first-time buyers should ask before signing any loan document.

These topics do more than bring traffic. They build trust. They show that your brand understands the customer’s situation, not just their wallet.

Make every message sound like a calm expert sitting beside the buyer

Home loan marketing often fails because it sounds too cold. Many lenders use stiff language that feels like paperwork. The customer already feels nervous. If your website sounds like a legal form, they will not feel closer to you.

Your tone should be calm, clear, and helpful. You do not need to oversimplify the loan itself, but you do need to explain it in human language. Instead of saying, “Applicants must comply with eligibility parameters subject to institutional underwriting,” say, “We check your income, credit history, current loans, and property details before approval.”

Simple language builds trust faster.

A customer should feel that your brand is easy to deal with before they ever speak to your team. If your marketing is clear, they will assume your process is clear. If your website is confusing, they will assume your loan process will be confusing too.

Your brand must become the safe choice, not just the cheap choice

Low rates can attract attention, but trust closes the deal. The problem with competing only on interest rates is that someone else can always go lower. Even worse, rate-focused marketing brings many customers who are only shopping for the lowest number.

These leads often compare endlessly, negotiate aggressively, and disappear without warning.

Trust-based marketing attracts a better customer.

This does not mean you should hide your rates or ignore price. It means you should place price inside a bigger story. Your message should make the customer feel that they are not just getting a loan. They are getting a smoother journey, a clearer process, better guidance, and fewer surprises.

A home loan customer wants to know what will happen next. They want to know how long approval may take. They want to know what documents they need. They want to know how much down payment they should plan for. They want to know what costs appear after approval. The more clearly you answer these questions, the safer your brand feels.

Show the process before asking for the application

One of the best ways to build trust is to show the full home loan process in simple steps. But do not present it as a cold checklist. Explain what happens at each stage and what the customer should do to avoid delays.

Start with the first conversation. Then explain eligibility checks, document collection, property review, loan offer, approval, signing, and disbursal. At each stage, tell the customer what to expect. This removes uncertainty.

When buyers understand the process, they feel more ready to act.

This also improves lead quality. A customer who knows the steps is less likely to drop off because of confusion. They come prepared. They bring better documents. They ask better questions. Your sales team spends less time explaining basics and more time closing real opportunities.

Make hidden costs clear before competitors use them against you

Home loan customers are scared of hidden costs. Even if your company is honest, many buyers assume lenders may have extra charges buried in the fine print. If you do not address this fear, it stays in the customer’s mind.

Talk openly about costs.

Explain processing fees, valuation charges, legal checks, insurance costs, stamp duty, registration, prepayment charges, and late payment fees where applicable. You do not have to scare people. You simply have to make them aware.

This creates a strong trust signal. Most brands avoid these topics because they fear it will reduce conversions. In reality, clear cost education often improves conversions because it makes your brand feel honest.

A serious buyer does not expect a home loan to have no costs. They expect the lender to be clear about them.

Your content must guide different types of home loan customers differently

Not every home loan customer has the same problem. A first-time buyer needs a different message from someone refinancing a loan. A salaried employee has different concerns from a business owner. A young couple buying their first apartment has different fears from an investor buying a second property.

If your marketing treats all home loan customers the same, your message becomes too general. General messages do not convert well.

You need customer segments.

This does not mean creating complicated campaigns for every small group. It means understanding the main types of buyers and creating content, ads, landing pages, and follow-up messages for each one.

First-time buyers need education and emotional support

First-time buyers are often excited but unsure. They may not know how much loan they can get. They may not understand how their monthly payment is calculated. They may be comparing rent versus buying. They may fear making a mistake that affects their future.

For this group, your marketing should feel like a guide.

Create pages and articles that explain home loan basics in plain words. Build calculators that help them estimate monthly payments. Share simple examples that show how loan amount, tenure, and rate affect the final cost. Offer downloadable guides that explain the documents needed before applying.

The goal is not to push them hard. The goal is to make them feel ready.

When a first-time buyer feels that your brand taught them what they needed to know, they are more likely to trust you when it is time to apply.

Refinancing customers need savings proof and timing advice

A refinancing customer already has a loan. They are not new to the process. Their main question is simple: “Will switching help me save enough money to make the effort worth it?”

Your marketing for this group must be direct and practical.

Show how refinancing can reduce monthly payments, shorten loan tenure, or lower total interest paid. But also explain when refinancing may not make sense. This honesty is important. If you tell everyone to refinance, your message feels like a sales pitch. If you explain both the benefits and the limits, your advice feels stronger.

Create tools that help people compare their current loan with a possible new one. Show examples of break-even points. Explain transfer fees, processing charges, and paperwork. Help them decide, not just apply.

Self-employed customers need confidence that they can qualify

Self-employed buyers often worry that lenders will treat them as risky. They may have strong income but irregular documents. They may not have a fixed salary slip. They may use business income, tax returns, bank statements, or profit records to prove eligibility.

This group needs content that removes doubt.

Explain what documents self-employed applicants may need. Show how lenders assess business income. Talk about common reasons applications get delayed. Give practical advice on preparing bank statements, tax records, and business proof before applying.

This kind of content can attract highly valuable customers because many lenders do not speak clearly to them. If your brand becomes the one that understands their situation, you can win trust early.

Existing customers need cross-sell messages that feel helpful, not pushy

Some of your best home loan customers may already know your brand. They may have savings accounts, credit cards, personal loans, business accounts, or insurance products with you. But many lenders fail to market home loans well to their existing base.

The key is to avoid sounding like you are simply pushing another product.

Use customer data wisely and ethically. If someone has steady income, a strong repayment record, and signs of home-buying interest, send them helpful content. Talk about planning for a first home, checking affordability, or understanding pre-approved loan options.

The message should feel like a useful next step, not a random promotion.

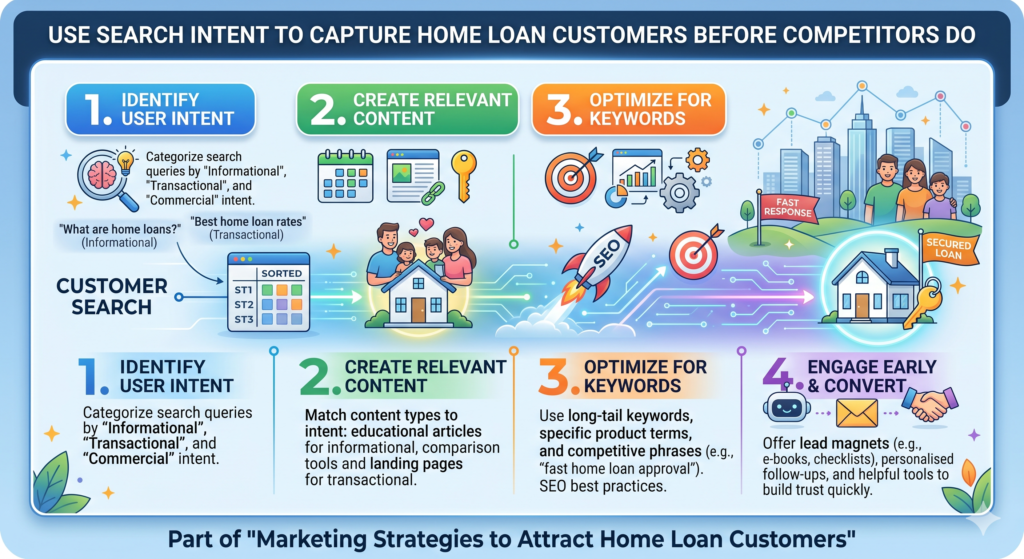

Use Search Intent to Capture Home Loan Customers Before Competitors Do

Search is one of the most powerful channels for home loan marketing because it catches people while they are actively looking for answers. But many lenders only target obvious keywords like “home loan,” “mortgage loan,” or “best home loan rates.” These keywords matter, but they are also crowded, expensive, and often too broad.

The smarter strategy is to target the full search journey.

A customer may begin with “how much home loan can I get,” then search “home loan documents required,” then “fixed vs floating home loan,” then “best home loan for first-time buyers,” and finally “apply for home loan.” If you only show up at the final stage, you are fighting every lender at the same time.

If you show up earlier, you build trust before the customer starts comparing.

Home loan SEO should be built around questions, not just keywords

People search in questions when they feel unsure. Home loans create a lot of uncertainty, so question-based content is a goldmine. These searches may not always have huge volume, but they often bring serious buyers who are moving closer to a decision.

Think about what people ask before they apply.

They want to know how much loan they can afford. They want to know what credit score is needed. They want to know whether they should choose a shorter or longer loan tenure. They want to know how much down payment they need.

They want to know whether they can get a loan with existing debt. They want to know how long approval takes.

Each question can become a strong content page.

But the page must not be thin. It should answer the question fully, clearly, and practically. A short 500-word article that repeats the same basic points will not build trust. The customer should leave the page feeling that they understand the topic better than before.

Match each page to one clear customer problem

A common SEO mistake is trying to answer too many things on one page. For example, a lender may create one article called “Everything About Home Loans” and stuff it with many topics. That can be useful as a guide, but it is not enough for strong search visibility or high conversion.

Each major customer problem deserves its own page.

A page on “how much home loan can I get” should focus deeply on eligibility, income, debt, credit score, down payment, loan tenure, and property value. A page on “home loan documents required” should focus on documents for salaried buyers, self-employed buyers, co-applicants, and property verification.

A page on “fixed vs floating home loan” should explain how each works, who each may suit, and what questions the buyer should ask before choosing.

This creates a stronger user experience. It also helps search engines understand the purpose of each page.

Use simple examples to make hard topics easy

Home loan topics can become dry very fast. Customers may lose interest if every page feels like a textbook. The best way to keep them engaged is to use simple examples.

For example, when explaining loan tenure, show how a longer tenure may reduce the monthly payment but increase total interest. When explaining down payment, show how a larger down payment may reduce loan size and future pressure. When explaining credit score, show how missed payments can hurt approval chances.

Examples make the advice easier to remember.

They also make your brand feel more human. The customer sees that you are not only giving information. You are helping them picture the decision in real life.

Local SEO can bring high-intent home loan customers from your service area

Home loans are often local decisions. Even if a lender works online, many customers still search with location-based terms. They may type “home loan agent near me,” “mortgage broker in [city],” “home loan for apartment in [area],” or “best bank for home loan in [city].”

If you serve specific cities, neighborhoods, or regions, local SEO should be a major part of your strategy.

Local pages can work very well when they are built properly. But they must not be copied and pasted with only the city name changed. That kind of content feels weak and often performs poorly. Each local page should speak to the real housing market, buyer needs, property types, and common questions in that area.

Build local pages that feel truly local

A strong local home loan page should explain the types of buyers you serve in that city. It should talk about common property types, popular buyer concerns, and the local buying process where relevant. It should include your office details if you have a branch there. It should explain how customers can get support.

The page should not feel like a doorway page created only for search engines. It should feel useful to a buyer in that location.

For example, a buyer in a high-cost city may care more about affordability, larger loan amounts, and co-applicant income. A buyer in a fast-growing suburb may care more about new developments, builder approvals, and first-home planning. A buyer in a smaller town may care more about document support and branch access.

When your local content reflects these real differences, it becomes more persuasive.

Treat your Google Business Profile like a conversion page

For local home loan searches, your Google Business Profile can be just as important as your website. Many buyers will see your profile before they visit your site. They will check reviews, photos, hours, location, call options, and questions.

Do not treat this profile as a basic listing.

Keep it updated. Add clear service descriptions. Use simple language. Add photos of the branch or team if relevant. Ask happy customers to leave honest reviews. Respond to reviews in a calm and professional tone. Answer common questions. Make it easy for people to call, book, or visit.

A strong profile can turn local search traffic into real leads.

Reviews should tell the story your ads cannot tell

Home loan customers trust other customers because they know the stakes are high. A good review does more than say “great service.” It explains what the customer was worried about and how your team helped.

Encourage customers to mention specific parts of the experience. Did your team explain the process clearly? Did you help them arrange documents? Did you respond quickly? Did you support them through approval? Did you help them understand repayment options?

Specific reviews are powerful because they feel real.

They also help future buyers see themselves in past customers. A first-time buyer will connect with a review from another first-time buyer. A self-employed person will trust a review from another business owner. A refinancing customer will pay attention to someone who saved money by switching.

Your landing pages must turn search traffic into serious leads

Getting search traffic is only half the job. The real goal is to convert that traffic into calls, form fills, appointments, or applications. Many home loan pages fail here because they are either too pushy or too vague.

A strong landing page should do three things.

It should make the offer clear. It should reduce fear. It should make the next step easy.

For a home loan customer, the next step should not always be “apply now.” Some visitors are not ready for that. They may prefer “check eligibility,” “estimate monthly payment,” “speak to a loan expert,” or “get a document checklist.” These softer calls to action can capture more leads earlier in the journey.

Give visitors more than one way to take action

Not every customer wants to fill a long form. Some want to call. Some want WhatsApp or chat. Some want to book a time. Some want to download a guide first. Some want to use a calculator before speaking to anyone.

Your landing page should support different comfort levels.

The ready buyer should see a clear apply option. The unsure buyer should see a simple eligibility check. The cautious buyer should see educational resources. The busy buyer should see a quick call booking option.

This does not mean cluttering the page with too many buttons. It means placing the right next step at the right point in the page.

At the top, offer a simple action like checking eligibility. In the middle, after explaining benefits and process, offer a call or consultation. Near the bottom, after answering common questions, offer application support.

Use forms that feel easy, not scary

Home loan forms can scare people away when they ask for too much too soon. If a visitor is just checking options, they may not want to share every financial detail immediately.

Start small.

Ask for only what you need to begin the conversation. Name, phone number, location, loan purpose, and rough income range may be enough for an early lead. You can collect deeper details later once trust is built.

Also explain what happens after the form is submitted. Tell the customer whether someone will call, how soon they can expect contact, and what information they should keep ready. This small detail reduces anxiety.

A form should never feel like a black hole.

Place trust signals near action points

When a customer is about to click, call, or submit a form, their doubts become stronger. This is the best place to show trust signals.

Place customer reviews near the form. Mention years of experience if true. Show lender partnerships if relevant. Add simple privacy reassurance. Explain that checking eligibility does not force them to accept a loan. Show that expert help is available.

Trust signals work best when they appear near the decision moment.

Do not hide them at the bottom of the page. Use them where they help the customer move forward.

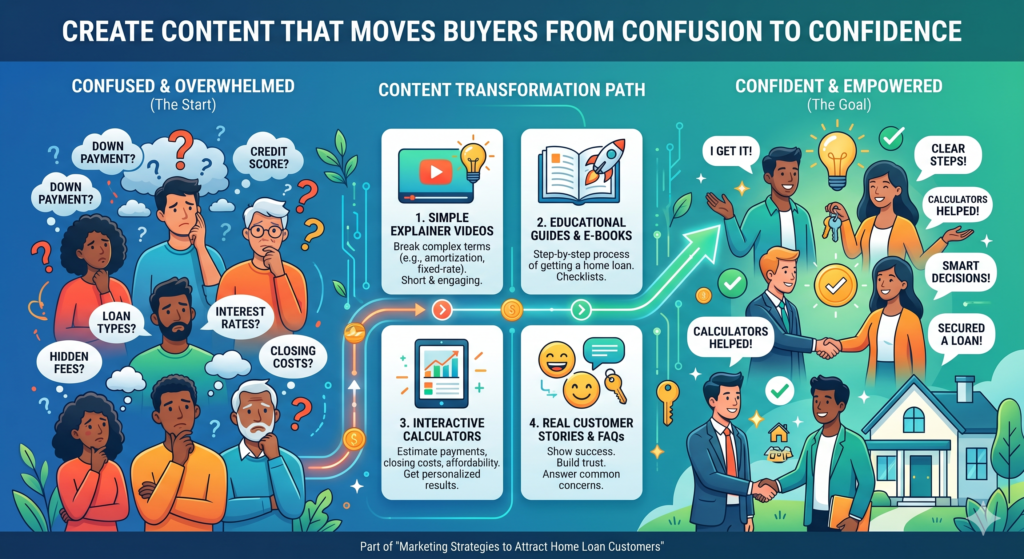

Create Content That Moves Buyers From Confusion to Confidence

Content is not just an SEO tool. In home loan marketing, content is a trust-building machine. The right content can educate buyers, reduce sales objections, improve lead quality, and shorten the decision time.

But the content must be built around the customer’s journey.

A person who just started thinking about buying a home needs different content from someone comparing loan offers. A person who is ready to apply needs different content from someone who was rejected before. Your content should move people step by step from confusion to confidence.

Top-of-funnel content should help customers understand their situation

At the early stage, buyers are not ready for a hard sales pitch. They are asking basic but important questions. They want to know whether buying makes sense, how much they can afford, how loans work, and what mistakes to avoid.

This is where educational content wins.

Write articles that help people think clearly. Talk about signs they may be ready to buy a home. Explain how to compare renting and buying. Show how monthly payments fit into a family budget. Discuss how credit history affects loan options. Explain why getting pre-approval before house hunting can save stress.

This type of content attracts people early. It also gives your brand the first chance to shape their thinking.

Teach before you ask for the lead

Many brands put lead forms too early. They ask for contact details before giving value. That may work with some ready buyers, but it can push away people who are still learning.

Give useful information first.

Then invite the reader to take the next step. For example, after an article on affordability, invite them to check their home loan eligibility. After a guide on documents, invite them to download a full checklist or speak with a document expert. After a post on first-time buyer mistakes, invite them to book a simple planning call.

This feels helpful, not aggressive.

When the customer feels helped, the lead becomes warmer.

Answer the questions buyers feel embarrassed to ask

Many home loan customers have questions they may not want to ask a banker directly. They may feel embarrassed about low savings, past credit issues, unstable income, or not understanding basic terms.

Your content should make these questions safe.

Write about whether someone can get a home loan with existing debt. Explain what happens if a credit score is not strong. Talk about whether a co-applicant can improve eligibility. Explain how lenders view job changes. Discuss what buyers can do if they do not have enough down payment yet.

These topics build a deep emotional connection because they speak to real fears.

A customer who feels seen is more likely to reach out.

Middle-of-funnel content should help customers compare options

Once buyers understand the basics, they start comparing. This is where they look at lenders, rates, loan types, fees, tenure, approval speed, customer service, and repayment flexibility.

Your content should help them compare without feeling lost.

Create comparison guides that explain what matters beyond the headline interest rate. Talk about total loan cost, fees, prepayment rules, customer support, processing time, and long-term flexibility. Explain what questions they should ask every lender before choosing.

This positions your brand as a trusted advisor.

Show customers how to compare loan offers the right way

Many buyers focus only on the interest rate. That is understandable, but it can lead to poor decisions. A slightly lower rate may not be the best deal if fees are high, support is poor, or terms are unclear.

Teach customers to compare the full offer.

Explain how to look at monthly payment, total interest, processing fees, insurance, prepayment rules, late fees, reset periods, and service quality. Use simple language. Give practical examples. Show that a good home loan is not just cheap on day one, but manageable over many years.

This type of content creates trust because it helps buyers avoid mistakes.

It also prepares them for better sales conversations. When they speak to your team, they already understand what matters.

Use case-based content for different buyer needs

Case-based content is powerful because it feels real. Instead of only explaining loan features, show how different types of buyers might think.

For example, write about how a young couple can plan for their first home loan. Explain how a self-employed designer can prepare income proof. Show how a family upgrading to a bigger home can manage loan overlap. Discuss how an existing borrower can decide whether refinancing is worth it.

These stories make your content more engaging.

They also help customers identify themselves. When they see their situation on your website, they feel that your brand understands them.

Bottom-of-funnel content should remove the final doubts before action

At the final stage, buyers are close to applying. But they may still hesitate. They may worry about rejection. They may fear hidden costs. They may be unsure about documents. They may want to speak to someone but feel nervous.

Your bottom-of-funnel content should remove these last barriers.

Create pages that explain exactly how to apply. Show what happens after application. Explain how long each step may take. List common reasons for delays and how to avoid them. Share customer stories. Answer common final questions.

This is where clarity converts.

Make your application page feel supportive

Many application pages are too cold. They simply say “Apply Now” and show a form. For a home loan, that is not enough.

The application page should reassure the customer.

Tell them what information they need. Explain that your team will guide them. Show the steps after submission. Add privacy reassurance. Mention that they can ask questions before moving forward. Include contact options for people who do not want to complete the form alone.

The page should feel like a doorway to help, not a trap.

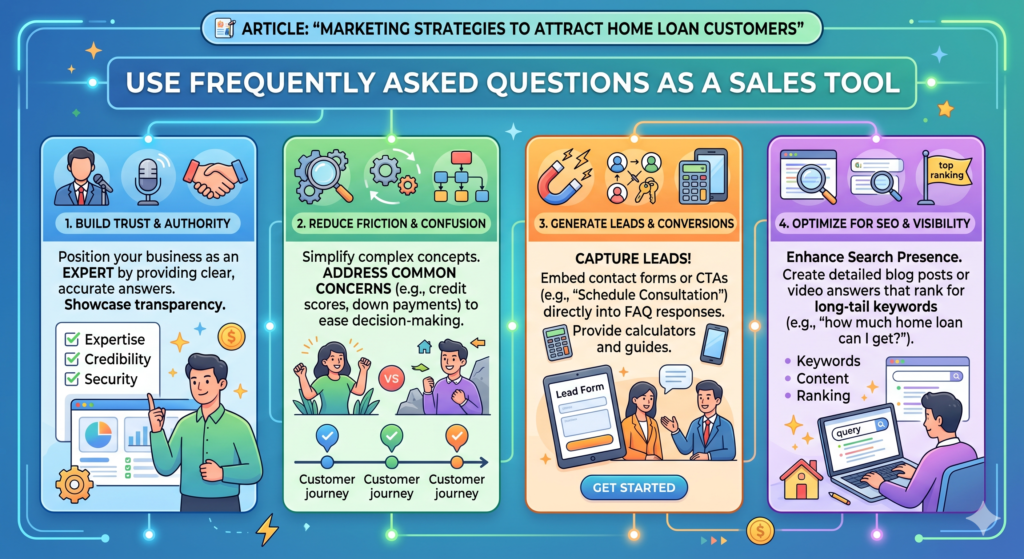

Use frequently asked questions as a sales tool

FAQs are often treated as filler, but they can be a strong conversion tool. The best FAQs answer the doubts that stop people from acting.

Do not write generic questions only.

Answer real concerns. What if my income is not fixed? Can I apply with my spouse? Will checking eligibility affect my credit score? What documents should I prepare? Can I repay early? What happens if the property is still under construction? How long does approval take? What if I already have another loan?

Each answer should be clear and honest.

A good FAQ section can reduce calls from unqualified leads and increase action from serious buyers.

Use Paid Ads to Capture Ready Buyers Without Wasting Budget

Paid ads can work very well for home loan marketing, but only when they are built with care. The mistake many lenders make is simple. They run broad ads to broad audiences and send everyone to the same basic page. Then they wonder why the cost per lead is high and the lead quality is poor.

Home loan ads are not like impulse-buy ads. You are not selling a low-cost product that people can buy in seconds. You are asking someone to take a major financial step. That means your paid ads must do more than grab attention. They must match the customer’s stage, answer the right worry, and lead them to a page that feels safe.

A good paid ad strategy does not chase every click. It filters for serious buyers.

Your goal is not only to get more leads. Your goal is to get leads who are more likely to qualify, respond, and move forward. This is where strategy matters.

Search ads should be built around high-intent home loan needs

Search ads are powerful because they catch people while they are actively looking. But not every search has the same value. Someone searching “what is a home loan” is in a different place from someone searching “home loan eligibility check” or “best home loan for first-time buyers.”

If you treat all searches the same, you will waste money.

Your search ads should be grouped by intent. Some ads should target people who are ready to apply. Some should target people comparing lenders. Some should target people checking eligibility. Some should target people looking for specific help, such as self-employed home loans, refinancing, or home loans with a co-applicant.

Each group should have its own message and landing page.

Write ad copy that speaks to the customer’s next step

A good home loan ad should not just say “Get a home loan today.” That is too broad. It does not speak to the reason the person searched.

If someone searches for eligibility, the ad should focus on checking eligibility. If someone searches for refinancing, the ad should focus on possible savings. If someone searches for first-time buyer help, the ad should focus on guidance. If someone searches for documents, the ad should offer a simple document checklist.

The more closely the ad matches the search, the more useful it feels.

This also improves the quality of the click. The person knows exactly what they are getting. They are less likely to land on the page and leave because the message feels wrong.

Do not send every paid click to the same page

Many lenders send all paid traffic to one home loan page. This is easy, but it is not smart.

A person looking for refinancing should not land on the same page as a first-time buyer. A self-employed applicant should not land on a generic salaried-buyer page. A person searching for eligibility should not land on a page that only talks about interest rates.

The landing page must match the ad.

This is one of the simplest ways to improve paid ad performance. When the customer clicks an ad that promises a clear answer, the page should continue that same promise. If the ad says “Check Your Home Loan Eligibility,” the page should focus on eligibility, what affects it, and how the check works. If the ad says “Compare Home Loan Options,” the page should help the user compare options and then invite them to speak to an expert.

Paid traffic is expensive. Every mismatch costs money.

Social ads should build trust before asking for an application

Social media ads work differently from search ads. On search, people are looking for a solution. On social, they are usually scrolling. They may not be ready to apply. They may not even be thinking about home loans at that moment.

This does not mean social ads cannot work. It means the message must be softer and smarter.

Instead of pushing “Apply Now” to cold audiences, use social ads to build awareness, educate buyers, and bring them into your funnel. Show helpful content. Offer simple tools. Share short videos. Promote guides. Retarget people who showed interest.

Social ads are best when they create trust first and sales later.

Use simple education ads for first-time buyers

First-time buyers spend a lot of time on social platforms. Many are not ready to apply yet, but they are thinking about buying a home. They may follow real estate pages, watch property videos, compare locations, or save posts about home design.

This is a good chance to reach them early.

Create ads that answer simple questions. Talk about how to know if you are ready to buy. Explain how much down payment may be needed. Show how monthly payments work. Share mistakes first-time buyers should avoid. Promote a free home loan readiness guide.

The goal is to make the customer stop and think, “This is useful.”

Once they engage, you can retarget them with stronger offers later.

Use retargeting to bring back serious visitors

Most home loan customers will not convert on the first visit. They may check your page, compare other lenders, talk to family, or wait until they have more documents ready. If you do not retarget them, you lose many good prospects.

Retargeting helps you stay visible after the first visit.

But the retargeting message should match what they viewed. If they visited an eligibility page, show them an ad about checking eligibility with expert help. If they used a calculator, show them an ad about planning a monthly payment. If they visited a refinancing page, show them an ad about comparing current loan cost with new options.

Retargeting should feel helpful, not annoying.

Do not show the same “Apply Now” ad again and again. Use different angles. Answer doubts. Offer proof. Invite action when the customer is ready.

Paid ads must be tracked beyond form fills

A big problem in home loan paid marketing is poor tracking. Many teams only measure cost per lead. That is not enough.

A cheap lead is not always a good lead. A lead may fill the form but never answer the phone. Another lead may answer but not qualify. Another may qualify but not submit documents. Another may get approved but not accept the offer.

If you only track form fills, you may optimize toward the wrong audience.

You need to track the full path from click to qualified lead, from qualified lead to application, from application to approval, and from approval to disbursal. This is how you know which campaigns actually bring business.

Connect marketing data with sales outcomes

Your ad platform may tell you which campaign brought the most leads. But your sales team knows which leads were serious. These two views must come together.

If a campaign brings many low-quality leads, reduce spend even if the cost per lead looks good. If another campaign brings fewer leads but more approvals, increase spend. If a keyword brings high-income buyers with strong documents, protect that keyword.

If a social audience brings curious people but few applicants, move it higher in the funnel and stop judging it only by direct applications.

Marketing should not be judged by surface numbers.

For home loans, the true value is in qualified applications and funded loans. When you track deeper, your budget becomes sharper.

Use call tracking because many home loan leads prefer to speak

Many home loan customers do not want to fill out a long form. They want to call and ask questions. If your ads drive phone calls but you do not track them properly, you may undercount your best campaigns.

Use call tracking where possible. Track which keyword, ad, or landing page drove the call. Also track call quality. Did the person ask serious questions? Did they have a property in mind? Did they discuss income? Did they book a follow-up? Did they submit documents later?

Calls can be some of the strongest home loan leads.

But they need the same attention as form leads. If calls are not answered fast, or if the staff sounds rushed, paid ad money is wasted.

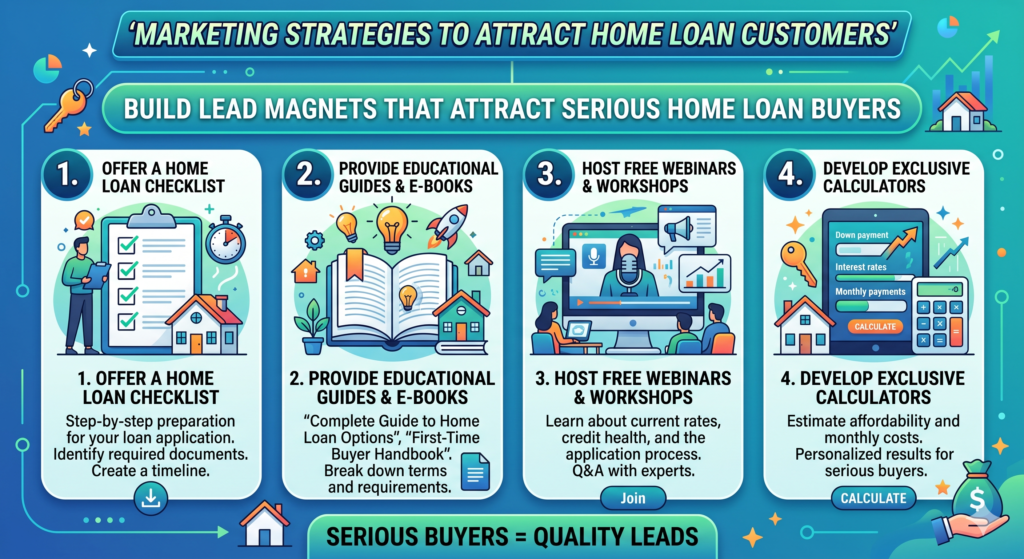

Build Lead Magnets That Attract Serious Home Loan Buyers

A lead magnet is something useful you give in exchange for contact details. In home loan marketing, lead magnets can work very well because buyers need help before they are ready to apply.

But the lead magnet must be practical.

A weak lead magnet is a generic PDF that says the same things every lender says. A strong lead magnet helps the customer make a real decision. It gives them clarity. It saves time. It makes them feel more prepared.

The best lead magnets do not attract random people. They attract people with real home loan intent.

Offer tools that help buyers understand affordability

Affordability is one of the biggest questions in home loans. People want to know how much they can borrow, what their monthly payment may look like, and whether buying now is wise. This is where tools can bring high-quality leads.

A simple calculator can be powerful if it is designed well.

But do not stop at showing numbers. Explain what the numbers mean. If someone enters income, down payment, and expected property cost, show a simple result with useful guidance. Tell them what may affect final approval. Explain why the number is only an estimate. Invite them to speak with an expert for a clearer view.

This turns a calculator into a lead path.

Make calculators easy enough for normal people to use

Many loan calculators feel too technical. They ask for too many details too early. They use terms the average buyer may not understand. This can scare people away.

Keep your calculator simple.

Ask for the few details needed to give a useful estimate. Use plain labels. Explain each field in simple words. Do not make the customer feel foolish if they do not know the exact interest rate or tenure yet. Give default examples. Let them adjust the numbers easily.

A good calculator should feel like a helpful conversation.

Once they see the result, give them the next step. For example, “Want to understand what this means for your home search?” or “Speak with a loan expert before you choose your budget.” This is softer and more useful than only saying “Apply now.”

Use calculator results to personalize follow-up

When someone uses a calculator, they are giving you useful signals. They may reveal their budget range, loan amount, income level, location, or buying stage. Use this information carefully to make follow-up more helpful.

Do not send the same email to every calculator lead.

If someone checks a small first-home loan, send beginner-friendly guidance. If someone checks a large loan amount, send content about approval strength and document readiness. If someone checks refinancing savings, send advice on comparing current loan terms. If someone checks eligibility but does not apply, send a simple explanation of what affects approval.

Personal follow-up feels more relevant.

It also shows the customer that you paid attention to their situation.

Create document checklists that reduce buyer stress

Documents are a major source of stress in home loan applications. Many buyers delay applying because they are not sure what they need. Others apply with missing documents and then get frustrated when the process slows down.

A document checklist can be a simple but powerful lead magnet.

It should not be a generic list. It should be split by buyer type. Salaried applicants need one kind of guidance. Self-employed applicants need another. Joint applicants need another. Property documents need separate attention.

This kind of checklist attracts serious buyers because people who care about documents are usually closer to action.

Explain why each document matters

Most checklists only name the documents. That is useful, but not enough. A better checklist explains why each document is needed.

For example, income proof helps the lender understand repayment ability. Bank statements show cash flow and financial behavior. Identity proof confirms the applicant. Property documents help confirm ownership and legal status. Tax records help support declared income.

When buyers understand why documents matter, they are more likely to prepare properly.

This reduces back-and-forth and improves the customer experience.

Turn document preparation into a service offer

A checklist can naturally lead to a support offer. After the customer downloads it, invite them to get help reviewing their documents before applying. This can be positioned as a simple readiness check.

This is a strong lead path because it feels useful.

Instead of saying, “Apply for a loan,” you are saying, “Let us help you avoid delays.” That is a lower-pressure offer, but it can lead to a serious application.

This is especially useful for self-employed buyers, first-time buyers, and people buying under-construction property. These customers often need more guidance and may value expert support.

Use buyer guides to build trust with early-stage customers

Not every lead magnet has to target buyers who are ready this week. Some should attract people who may buy in the next few months. These leads are valuable because you can nurture them before competitors reach them.

A first-time home buyer guide can be a strong asset.

It can explain budgeting, loan eligibility, down payment planning, credit score, documents, property search, pre-approval, and final application. But it must be written in simple language. It should feel like a friendly guide, not a bank brochure.

The guide should help people feel ready.

Make the guide specific to one audience

A broad guide called “Home Loan Guide” may attract some people, but specific guides often perform better. Create guides for first-time buyers, self-employed buyers, newly married couples, families upgrading homes, and people planning to refinance.

Specificity makes the guide feel more personal.

A self-employed person is more likely to download “Home Loan Guide for Self-Employed Buyers” than a general loan guide. A first-time buyer is more likely to trust a guide that speaks directly to their fear of making a mistake.

The more specific the guide, the easier the follow-up becomes.

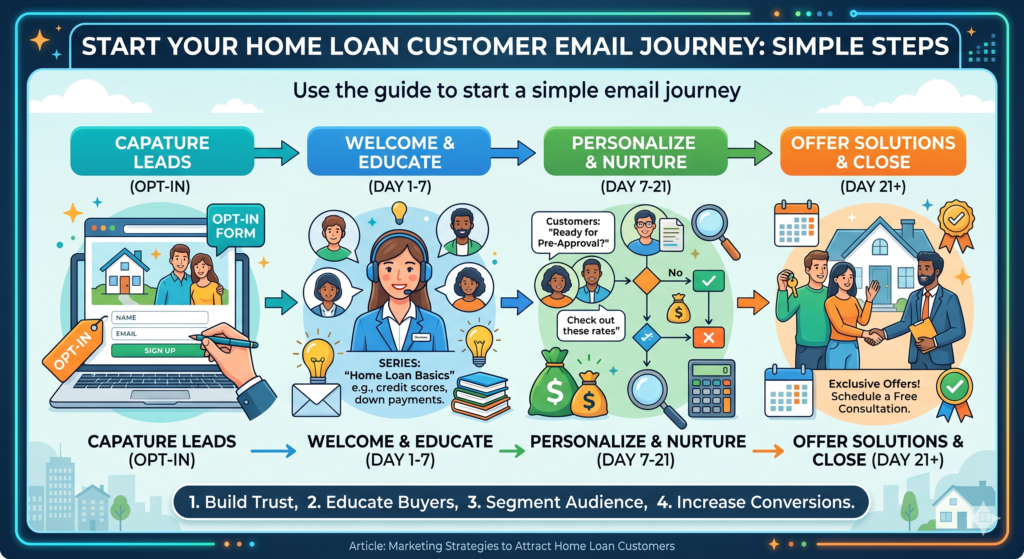

Use the guide to start a simple email journey

After someone downloads a guide, do not send only one sales email and stop. Build a short journey that helps them move forward.

The first email can deliver the guide and explain how to use it. The next email can help them understand affordability. Another can explain documents. Another can show common mistakes. Another can invite them to check eligibility or speak to a loan expert.

This works because it builds trust over time.

Home loan decisions often take weeks. A helpful email journey keeps your brand present without pressure.

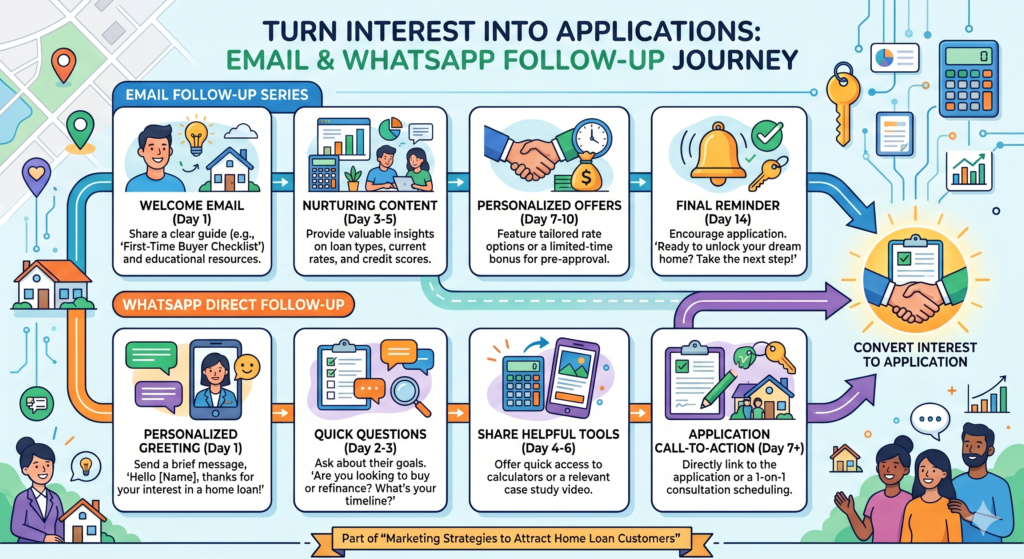

Use Email and WhatsApp Follow-Up to Turn Interest Into Applications

Many home loan leads are lost not because the customer was not interested, but because follow-up was weak. Someone fills a form, downloads a checklist, uses a calculator, or calls once. Then they get a dull message, a late call, or no useful next step.

That is a major waste.

Home loan follow-up must be fast, clear, and helpful. It should not feel like chasing. It should feel like guidance.

The customer may be busy. They may be nervous. They may need to talk to family. They may be comparing offers. Your follow-up should help them make progress.

Speed matters because buyers often contact more than one lender

When a customer submits a home loan inquiry, there is a good chance they have contacted other lenders too. If your team responds slowly, another lender may shape the conversation first.

Fast follow-up does not mean sounding desperate. It means being useful while the customer’s interest is fresh.

A quick message should confirm that you received the inquiry, explain the next step, and make it easy to respond. If a call is needed, give a clear reason for the call. If documents are needed, explain which ones and why.

The first message should reduce uncertainty

The first follow-up message should not be a cold sales line. It should make the customer feel safe.

For example, it can say that your team will help them understand eligibility, possible loan amount, documents needed, and next steps. It can also tell them they do not need to decide right away. This lowers pressure and increases response.

The customer should feel that replying will help them, not trap them.

That small change can improve lead response rates.

Do not ask for too much too soon

Many lenders lose leads by asking for too many documents or details in the first message. A new lead may not be ready to share salary slips, tax records, bank statements, or property papers immediately.

Start with a simple conversation.

Ask where they are in the journey. Are they still planning, already searching for a property, comparing lenders, or ready to apply? This helps you guide them better. Once trust is built, the customer is more likely to share deeper information.

Home loan sales works best when the customer feels respected.

Segment follow-up by buyer stage and buyer type

Every lead should not get the same follow-up. A person who used an EMI calculator is not the same as someone who asked for a callback. A refinancing lead is not the same as a first-time buyer. A self-employed buyer is not the same as a salaried buyer.

Segmenting follow-up makes your messages more useful.

If someone is early-stage, send education. If someone is comparing lenders, send comparison help. If someone is ready to apply, send document support. If someone has gone silent, send a helpful reminder with a clear next step.

Early-stage leads need patience and guidance

An early-stage buyer may not apply right away. That does not make them a bad lead. It means they need nurturing.

Send them content that helps them prepare. Explain how to improve eligibility. Share tips on saving for down payment. Help them understand credit score. Offer a simple planning call.

Do not push too hard.

If you pressure early-stage leads, they may unsubscribe or ignore you. If you help them, they may come back when ready.

Ready buyers need clarity and momentum

A ready buyer should not be left waiting. They need a clear path.

Tell them what details are needed, what documents to prepare, how long the next step may take, and who will guide them. Give them one simple action at a time.

Momentum matters.

If the process feels slow or unclear, the buyer may switch to another lender. Your follow-up should keep the journey moving without making the customer feel rushed.

WhatsApp can work well when it feels personal and useful

For many home loan customers, WhatsApp feels easier than email. It is quick, familiar, and direct. But it can also feel intrusive if used poorly.

The key is to keep WhatsApp messages short, helpful, and respectful.

Do not flood the customer with promotions. Use WhatsApp to answer questions, share checklists, confirm appointments, remind them of documents, and guide them through next steps.

Use WhatsApp for service, not spam

A good WhatsApp message should feel like help from a real person. It should be clear and specific.

Instead of sending “Apply for home loan now,” send a message that says you can help them check eligibility, understand possible loan amount, and prepare documents before applying. Invite them to reply with a simple answer about their buying stage.

This creates a conversation.

Conversations convert better than blasts.

Make it easy for customers to restart the conversation

Some buyers go silent because life gets busy. They may still be interested, but they are not ready right now. Your follow-up should make it easy to come back.

Send occasional useful messages, not constant reminders. For example, share a short note about documents, affordability, or common mistakes. End with a simple invitation to reply when they want help.

The tone should be calm.

A home loan customer should never feel hunted. They should feel supported.

Use Video Marketing to Make Home Loans Feel Less Confusing

Home loans can feel heavy when explained only through text. Many customers do not want to read long policy pages or complex guides before they understand the basics. They want someone to explain things in a simple way, the same way a trusted advisor would explain it across a table.

That is why video can be a powerful tool for attracting home loan customers.

Video makes your brand feel more human. It allows people to see faces, hear tone, and understand ideas faster. A short video can explain a topic that may take a long article to cover. More importantly, video helps reduce fear. When a customer sees a calm expert explaining the process in plain language, the loan starts to feel less scary.

But video should not be made only for views. It should be made to answer real questions and move people closer to action.

Create short videos around the questions buyers ask before they apply

The best home loan videos are not fancy. They are useful. A simple video shot clearly, with a real expert speaking in plain words, can often work better than a polished ad that says very little.

Start with the questions buyers already ask your sales team.

What documents do I need? How much loan can I get? What affects my eligibility? How does my credit score matter? Should I choose a shorter or longer tenure? Can I apply with my spouse? What happens after I submit my application? How long does approval take?

Each of these questions can become a short video.

The goal is to make the customer feel smarter after watching. When your videos help people understand the process, they begin to trust your brand before speaking with your team.

Keep each video focused on one clear problem

A common mistake is trying to explain everything in one video. That usually makes the video too long and too hard to follow. Home loan customers are already dealing with many moving parts. Your video should make one thing easier, not add more confusion.

For example, do not create one long video called “Everything You Need to Know About Home Loans” and expect it to work everywhere. Instead, create shorter videos with one clear idea. One video can explain eligibility. Another can explain documents.

Another can explain how monthly payments work. Another can explain mistakes first-time buyers should avoid.

This makes each video easier to watch, easier to share, and easier to place on the right page.

A video about documents should appear on your document checklist page. A video about eligibility should appear on your eligibility page. A video about refinancing should appear on your refinancing page. This way, the video supports the customer at the exact moment they need help.

Use a calm and friendly tone instead of sounding like an ad

Home loan videos should not sound like loud sales commercials. The customer is making a serious decision. They do not need hype. They need clarity.

Speak slowly. Use simple words. Avoid lender language that normal people do not use every day. Explain one idea at a time. Use examples. Repeat key points naturally, but do not sound scripted.

The person in the video should feel like a guide, not a salesperson.

This matters because customers are sensitive to pressure. If the video feels too pushy, they may leave. If it feels helpful, they may keep watching, explore more pages, and reach out when ready.

Use customer story videos to build stronger proof

Customer stories are one of the strongest forms of home loan marketing. A real buyer explaining how your team helped them can do more than a long sales page. This is because home loan customers want proof from people like them.

A good customer story should not only say the service was good. It should show the journey.

What was the customer worried about? Were they a first-time buyer? Were they unsure about documents? Were they self-employed? Were they comparing lenders? Did they need fast approval? Did they need guidance at each step?

The more specific the story, the more useful it becomes.

Focus on the before and after journey

A strong customer story has a clear before and after. Before working with your brand, the customer had a worry, delay, question, or goal. After working with your brand, they had clarity, support, approval, savings, or peace of mind.

This structure makes the story easy to follow.

For example, a first-time buyer may say they did not understand how much they could afford. Your team helped them check eligibility, understand documents, and plan the loan amount. A self-employed customer may say they were worried about income proof.

Your team helped them prepare the right papers and avoid delay. A refinancing customer may say they wanted to know if switching was worth it. Your team helped them compare the cost and make a clear choice.

These stories do not need to be dramatic. They need to be real.

Real stories help future buyers picture their own path.

Place story videos near decision points

Customer stories should not sit only on a testimonial page that few people visit. Place them where they can support action.

Put first-time buyer stories on first-time buyer pages. Put self-employed customer stories on self-employed loan pages. Put refinancing stories on refinancing pages. Put short review clips near forms and call booking sections.

This gives buyers proof at the moment they may be hesitating.

A customer who is about to submit a form may still wonder, “Can I trust this company?” A story from someone with a similar need can reduce that doubt.

Use live sessions and webinars to attract serious buyers

Home loan webinars can work very well when the topic is specific and useful. Many people are willing to attend a short session if it helps them make a better home buying decision.

The key is not to make the webinar sound like a sales pitch.

Make it feel like a helpful class. Teach people how to prepare for a home loan, how to avoid common mistakes, how to understand affordability, or how to compare loan offers. At the end, invite attendees to book a personal consultation or eligibility check.

This builds trust at scale.

Choose webinar topics that match real buyer anxiety

The best webinar topics come from buyer fear. People attend when the topic promises to remove a worry.

A session on “How to Know If You Are Ready for a Home Loan” can attract early-stage buyers. A session on “How First-Time Buyers Can Avoid Home Loan Mistakes” can attract serious new buyers. A session on “Home Loan Documents Explained in Simple Words” can attract people close to applying.

A session on “When Refinancing Your Home Loan Makes Sense” can attract existing borrowers.

Each topic should promise one clear outcome.

After attending, the customer should feel they understand something important.

Follow up after the session with a clear next step

A webinar is only valuable if you follow up well. Many brands run sessions, collect attendees, and then send a weak thank-you message. That wastes the opportunity.

After the session, send a short summary, a useful resource, and one simple next step. Invite attendees to check eligibility, review documents, use a calculator, or speak to a loan expert. Make the follow-up match the session topic.

If the webinar was about documents, offer a document readiness review. If it was about affordability, offer an eligibility call. If it was about refinancing, offer a loan comparison.

This keeps the journey natural.

Build Partnerships That Put Your Brand in Front of Home Buyers Earlier

Home loan customers often speak to several people before they speak to a lender. They speak to real estate agents, builders, property portals, financial advisors, lawyers, accountants, employers, friends, and family. These people shape the buyer’s thinking early.

That means partnerships can become a strong source of home loan leads.

But partnership marketing must be done carefully. It should not feel like a backroom referral machine. It should feel like a better support system for the buyer. The best partnerships help customers move through the home buying process with less stress.

When done well, partnerships can bring high-intent leads because the buyer is already in motion.

Partner with real estate agents without becoming too dependent on them

Real estate agents are often close to buyers at the right time. They know who is viewing homes, who is comparing budgets, and who may need financing soon. A strong relationship with agents can bring steady referrals.

But you should not rely only on agents. You also need your own brand, your own content, and your own lead system. Otherwise, your growth depends too much on other people’s pipeline.

The smart approach is to make agents part of a wider strategy.

Help agents serve their buyers better. Give them simple loan education materials. Offer quick eligibility support. Create co-branded guides where appropriate. Make it easy for them to refer buyers who need help understanding finance before choosing a property.

Give agents resources that make their job easier

Agents want buyers who are serious and financially ready. If a buyer does not know their budget, the agent may waste time showing properties that are not a good fit. You can help solve this problem.

Create simple resources agents can share with buyers. These may include affordability guides, eligibility check pages, document checklists, and home buying readiness content. The agent benefits because the buyer becomes clearer. You benefit because your brand enters the conversation early.

This is better than simply asking agents for leads.

When you make their work easier, they have a reason to keep sending people your way.

Keep the buyer experience clean and transparent

Partnership referrals can lose trust if the buyer feels pushed or passed around. Make the process clear. If an agent refers someone, the customer should understand why they are being introduced and what help they will receive.

Your first contact should be helpful, not aggressive.

Say that you can help them understand loan eligibility, possible budget, documents, and next steps. Do not make them feel they are being forced into one lender or one product. Trust is fragile in financial decisions.

A clean referral experience protects both your brand and the partner’s reputation.

Work with builders and developers to reach buyers at the property decision stage

Builders and developers can be strong partners because their buyers often need financing support. This is especially true for new projects, under-construction homes, and first-time buyers.

But again, the goal should be buyer support, not just lead capture.

A buyer considering a property may need to understand payment schedules, loan approval timing, construction-linked payments, documents, and total cost. If your brand can explain these clearly, you become useful at a critical moment.

Create project-specific finance guides where possible

If you work with builders or developers, create simple finance guides for specific projects or property types. Explain how loan approval may work, what documents are usually needed, what the payment stages look like, and what buyers should check before committing.

This can reduce confusion for buyers and improve lead quality.

The guide should be clear that final approval depends on lender checks and customer eligibility. Avoid making promises that may not apply to every buyer. Your role is to guide, not overpromise.

When buyers see that you are helping them understand the full financial picture, they are more likely to trust you.

Offer buyer education sessions for project launches

Project launches often attract interested buyers who are still unsure about affordability. Instead of only placing a desk at the event, offer short education sessions.

Explain how buyers can estimate their budget, prepare documents, and avoid delays. Answer common questions in simple language. Invite buyers to book a personal eligibility discussion.

This makes your presence feel valuable.

You are not just another booth. You are the finance expert helping people make a better decision.

Build referral relationships with accountants, financial planners, and employers

Some of the best home loan referrals can come from professionals who already understand the customer’s financial situation. Accountants may know when a self-employed client is planning to buy property. Financial planners may know when a family is preparing for a large purchase. Employers may offer home loan education as part of employee benefits.

These relationships can bring strong leads because trust already exists.

The customer may be more open to your advice when they are introduced by someone they already rely on.

Create simple referral education for professional partners

Professional partners do not need a hard sales pitch. They need to know when your service can help their client or employee.

Explain the signs that someone may need home loan guidance. These could include planning to buy a first home, wanting to refinance, preparing income documents, improving credit readiness, or comparing loan options.

Give partners a simple way to refer people.

Also give them content they can share. For example, an accountant may share a self-employed home loan document guide. An employer may share a first-home planning webinar. A financial planner may share a refinancing comparison guide.

This makes the referral feel useful and natural.

Respect the partner’s trust with the customer

When a referral comes from a trusted partner, you are borrowing that trust. Do not damage it with pushy sales behavior.

Respond quickly. Be clear. Give honest advice. Do not pressure the customer. Keep the partner informed only where appropriate and with respect for privacy.

A good referral experience creates more referrals.

A bad one closes the door.

Use Social Proof to Make Your Home Loan Brand Feel Safer

Home loan customers want proof. They want to know that other people trusted you and had a good experience. They want to see that your team can handle real situations, not just write nice promises on a website.

This is where social proof matters.

Social proof includes reviews, testimonials, case stories, ratings, customer videos, partner mentions, and even simple proof of experience. But it must be real and specific. Generic praise does not carry much weight.

A review that says “good service” is fine. A review that says “they helped me understand my documents and guided me through my first home loan” is much stronger.

Collect reviews that explain the customer’s situation

The best reviews tell a small story. They show who the customer was, what they needed, and how your team helped.

To collect better reviews, guide customers after a successful loan journey. Do not tell them what to say. Instead, ask them to share what they were trying to do, what concern they had, and what part of the service helped most.

This leads to more useful reviews.

A future buyer will connect with a review when it sounds like their own situation. First-time buyers want to hear from first-time buyers. Self-employed applicants want to hear from self-employed applicants. Refinancing customers want to hear from people who switched and saved.

Ask for reviews at the right moment

Timing matters. The best time to ask for a review is when the customer has reached a positive point in the journey. This may be after approval, after disbursal, after moving into the home, or after a helpful support experience.

Do not wait too long.

When the feeling is fresh, the customer can give more detail. If you wait months, they may only write a short generic line.

Make the review process simple. Send a clear link. Explain that their honest feedback helps other buyers make a better decision. Keep the request warm and respectful.

Turn strong reviews into content assets

A good review should not stay hidden on one platform. With permission, use strong reviews across your marketing.

Place them on landing pages, local pages, email journeys, social posts, and sales materials. Match each review to the right audience. A review about quick document help should appear near document-related content.

A review about first-time buyer support should appear on first-time buyer pages. A review about refinancing should appear on refinancing pages.

This makes proof more relevant.

Relevant proof converts better than random praise.

Create case studies that show how your team solved real problems

Case studies are longer than reviews and can be very persuasive. They allow you to show how your team helped a customer through a real journey.

A case study does not need to reveal private details. You can protect customer privacy while still showing the problem, process, and result.

The key is to make it useful for future customers.

Focus each case study on one clear challenge

Do not write vague case studies that only say the customer got a loan. Make each one about a specific challenge.

For example, one case study can focus on a self-employed buyer who needed help preparing income documents. Another can focus on a first-time buyer who did not know how much they could afford.

Another can focus on a family that wanted to refinance but needed to understand whether the savings were worth the fees. Another can focus on a buyer who needed guidance through property document checks.

Each story should teach something.

When a customer reads it, they should feel, “This company has handled situations like mine.”

Make the process the hero

In home loan case studies, do not only highlight the final approval. Highlight the process.

Show how your team listened, reviewed the situation, explained options, helped with documents, answered questions, and guided the buyer step by step. This is what customers care about.

Approval is important, but peace of mind is often what they remember.

When you show the process, you show the value of choosing your brand.

Use trust signals without making the page feel crowded

Trust signals are important, but too many badges, logos, claims, and reviews can make a page feel messy. The goal is not to shout proof from every corner. The goal is to place proof where it helps the customer decide.

Use proof near moments of doubt.

Place reviews near forms. Place case stories near service explanations. Place ratings near local contact sections. Place partner mentions where they support credibility. Place privacy reassurance near lead capture forms.

Keep proof specific and easy to believe

Avoid claims that sound too big unless you can clearly support them. Saying “the best home loan provider” may feel empty. Saying “helping first-time buyers understand eligibility, documents, and loan options” feels more believable.

Specific proof is stronger than broad claims.

Customers are careful with financial decisions. They can sense when marketing sounds exaggerated. Keep your proof grounded, clear, and real.

Build a Strong Website Experience That Makes Home Loan Buyers Feel in Control

Your website is not just a place where people read about your home loan service. It is often the first serious experience they have with your brand. Before they call your team, before they visit your branch, before they share documents, they judge you through your website.

If the site feels slow, unclear, hard to use, or too sales-heavy, the buyer may leave without saying anything.

This is especially true in home loan marketing because the customer is not making a small choice. They are making a long-term financial decision. If your website feels confusing, they may assume your loan process will also be confusing. If your website feels clear and helpful, they are more likely to believe your team will guide them well.

A strong home loan website does not only look good. It helps people think better, compare better, and act with more confidence.

Your home loan page should answer the buyer’s real questions in the right order

Many home loan pages are built around the lender’s needs, not the customer’s needs. They start with product features, then show a rate, then push the visitor to apply. But most buyers need a softer and clearer path.

A strong page should follow the way a buyer thinks.

First, the visitor needs to know whether the loan is right for them. Then they need to understand the main benefits. Then they need to know how eligibility works. Then they need to understand costs, documents, process, support, and next steps. Only after that should the application feel natural.

The page should feel like a guided conversation.

Start with clarity, not cleverness

The top of the page must be clear within seconds. A visitor should understand what you offer, who it is for, and what they can do next. Do not use clever slogans that sound nice but say little.

A simple opening works better.

Tell people that you help home buyers understand eligibility, compare options, prepare documents, and move through the loan process with less stress. This kind of message speaks to what the customer wants. They want a loan, yes. But they also want guidance, safety, and clarity.

Your first call to action should also be simple. It may invite them to check eligibility, estimate their monthly payment, speak to a loan expert, or start an application. The best choice depends on the visitor’s stage, but the language must feel easy.

Explain benefits through customer outcomes

Do not only say that you offer fast processing, flexible tenure, or competitive rates. Explain what those things mean for the customer.

Fast processing means they can move ahead with their property plan with less waiting. Flexible tenure means they can choose a repayment plan that fits their monthly budget. Clear document support means they can avoid delays. Expert guidance means they do not have to figure everything out alone.

This is an important copywriting rule.

Features are what you offer. Outcomes are why the customer cares.

A home loan customer is not excited by internal process terms. They care about getting approved smoothly, planning payments safely, and avoiding bad surprises.

Your website should make comparison easier, not harder

Home loan customers compare. They compare rates, lenders, fees, approval time, advice quality, and reviews. If your website does not help them compare, they will leave and do that comparison elsewhere.

You should not fear comparison. You should guide it.

When you teach buyers how to compare loan options, you become part of their decision process. You also shift the conversation away from rate alone and toward total value.

Create a simple comparison guide on your site

A comparison guide can help buyers understand what to check before choosing a home loan. It should explain that the lowest rate is important, but it is not the only factor. Buyers should also look at processing fees, prepayment terms, loan tenure, customer support, document support, approval steps, and long-term repayment comfort.

This does not need to be written as a long list. It can be explained in short sections with examples.

For example, explain that a low monthly payment may feel good today, but a very long tenure can increase total interest. Explain that a low rate may not feel as attractive if the process is slow or the terms are unclear. Explain that a lender who helps you prepare documents well can save time and stress.

This kind of education builds trust because it helps the customer make a smarter choice.

Show where your brand fits without attacking competitors

You do not need to insult other lenders to win trust. In fact, negative marketing can make financial brands look less reliable.

Instead, explain your strengths in a calm way.

If your strength is guidance, show how your team supports customers through eligibility, documents, and approval. If your strength is speed, explain what helps you move faster and what customers can do to avoid delays.

If your strength is local knowledge, show how you help buyers in specific areas. If your strength is self-employed applicant support, explain that clearly.

Customers do not need drama. They need reasons to believe.

Your site speed and mobile experience can affect lead quality

Many home loan searches happen on mobile. A customer may search while traveling, during lunch, after seeing a property, or while talking with family. If your page loads slowly or looks messy on a phone, you may lose the lead before your message is even seen.

This is not just a technical issue. It is a trust issue.

A slow website can make your brand feel careless. A broken form can make the buyer feel unsafe. Small buttons, crowded text, and hard-to-read pages can make the whole process feel tiring.

Design mobile pages for busy buyers

Mobile pages should be easy to scan. Paragraphs should be short. Headings should be clear. Forms should be simple. Buttons should be easy to tap. Phone and WhatsApp options should be visible where appropriate.

The buyer should not have to pinch, zoom, hunt, or struggle.

Remember that many visitors may be checking your site while doing something else. They may not have time to read everything. Help them find the next step quickly. Give them enough information to trust you, but do not bury action points under heavy blocks of text.

A good mobile page feels calm and easy.

That feeling can carry into the customer’s view of your service.

Test your forms like a real customer

A form may look fine to your team but feel annoying to a customer. Test it on a phone. Try filling it out with one hand. Check whether the fields are clear. Check whether error messages are helpful. Check whether the thank-you message explains the next step.

Small form problems can hurt conversions.

If a buyer submits a form and receives no clear confirmation, they may wonder if it worked. If the form asks for too much information, they may quit. If the form has unclear labels, they may enter wrong details.

A home loan form should feel like the start of support, not the start of paperwork.

Your website should build trust with transparency

Transparency is one of the strongest advantages a lender can show online. Buyers fear hidden charges, unclear terms, delays, and rejection. Your website should reduce these fears before they grow.

This does not mean giving every legal detail on every page. It means explaining important points in plain words and making help easy to access.

Explain what can affect approval

Many buyers think approval depends only on income. In reality, several factors can matter, including credit history, current debt, employment type, age, property details, down payment, and document strength.

Explain these factors simply.

This helps customers understand why one person may qualify for a different amount than another. It also helps them prepare better. When buyers understand the approval process, they are less likely to feel confused or upset if more documents are needed.

Clear education can also protect your sales team from repeated basic questions.

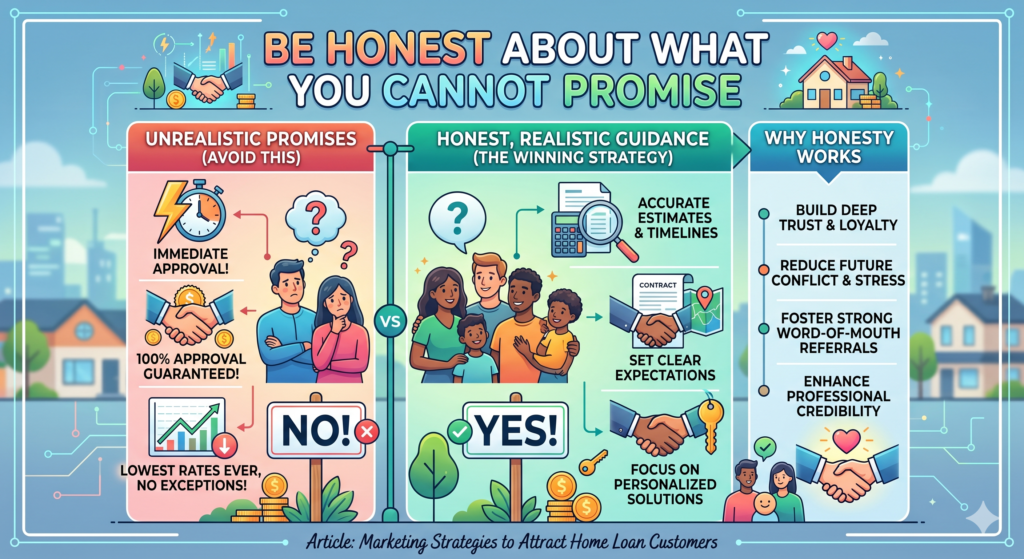

Be honest about what you cannot promise

Home loan marketing should never overpromise. Do not promise guaranteed approval if approval depends on checks. Do not promise the lowest rate for everyone if rates vary by profile. Do not promise instant disbursal if property and document review take time.

Honest language may seem less exciting, but it builds stronger trust.

You can still sound confident. Say that your team will help customers understand their options, prepare documents, and move through the process as smoothly as possible. That is believable. That feels safe.

In financial marketing, believable beats flashy.

Conclusion:

Attracting home loan customers is not about shouting the lowest rate the loudest. It is about helping people feel safe, clear, and ready during one of the biggest choices of their lives. The lenders that win are the ones that educate before selling, answer doubts before they become objections, and guide buyers at every step.

Comments are closed.